In the volatile theater of Wall Street commentary, few voices are as polarizing or as widely followed as Jim Cramer's. His latest proclamation on Tesla, however, cuts through the typical noise surrounding quarterly deliveries and EV price wars, reframing the entire investment thesis. Following the company's recent August 8th "Robotaxi" unveiling event, Cramer delivered a striking synopsis, urging investors to see beyond the carmaker label and recognize a transformative tech play.

Cramer's Pivot: From Car Company to Robotics Powerhouse

The CNBC host's emphatic shift in perspective is captured in a single, repeated directive: "buy, buy, buy." Cramer argued that Tesla's core narrative has fundamentally changed, stating, "Turns out it’s actually a robotics and Cybercab company." This analysis suggests the market is undergoing a significant re-rating, moving Tesla from the traditional automotive sector into the high-multiple realm of artificial intelligence and automation. His metaphor of Tesla being "the paper that turned into scissors in one session" underscores a perception of sudden and decisive strategic superiority gained through the Robotaxi reveal, potentially cutting through competitor narratives.

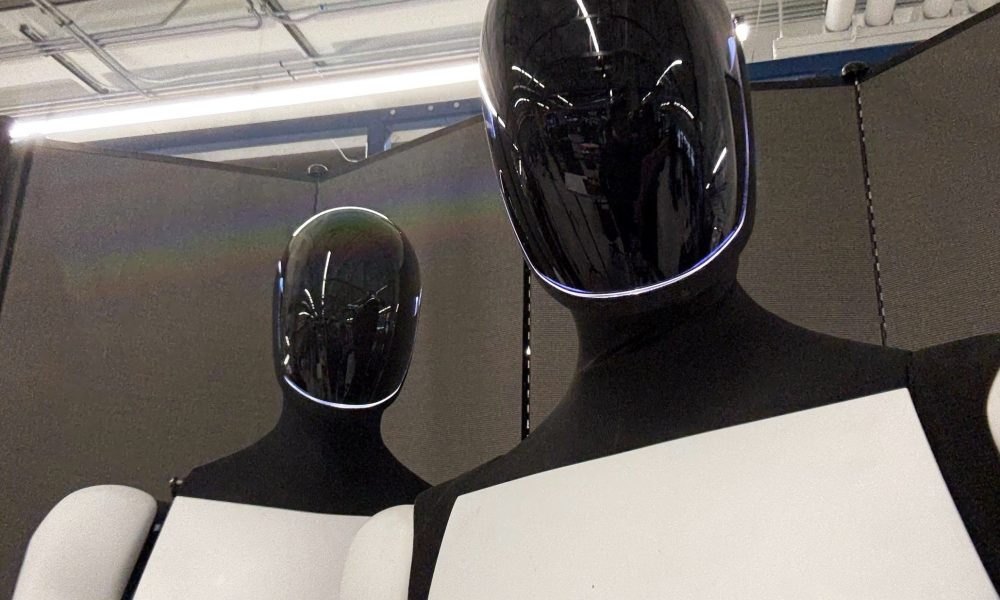

The Strategic Weight of the Cybercab and Optimus

This isn't merely speculative hype. Cramer's thesis is anchored in the tangible, dual-pronged technological offensive Tesla showcased. The dedicated Cybercab platform represents a pure-play bet on autonomous ride-hailing, a service with a vastly different financial model—recurring revenue, high asset utilization—than vehicle sales. More profoundly, it is intrinsically linked to the progress of Tesla's humanoid robot, Optimus. The event demonstrated that the same foundational AI and robotics stack driving the company's Full Self-Driving (FSD) ambitions is being leveraged to create a general-purpose automaton. This convergence positions Tesla not just as a player in transportation, but as a architect of versatile robotic systems.

The implications of this are monumental. If Tesla can successfully scale and commercialize Optimus, its addressable market explodes beyond automotive into manufacturing, logistics, and even consumer assistance. The company transforms from selling discrete vehicles to potentially leasing fleets of autonomous cabs and licensing robotic workforce solutions. This vision justifies a premium valuation disconnected from near-term auto sector margins, as investors begin to price in these nascent, high-growth software and service opportunities.

Implications for Tesla Owners and Investors

For Tesla owners, Cramer's spotlight on robotics validates the long-term ecosystem they've bought into. Their vehicles are the rolling data-collection nodes and early-access platforms for the AI that will power everything else. For investors, the commentary highlights a critical bifurcation in analysis. Evaluating Tesla solely on quarterly delivery numbers is becoming an increasingly myopic view. The investment debate must now aggressively factor in the monetization timeline for FSD, the Robotaxi network, and Optimus. This shift brings higher potential rewards but also greater risk and volatility, as these technologies remain unproven at scale. The stock will likely trade less on current auto P/E ratios and more on narratives of technological disruption and total addressable market capture in robotics—a sector where Tesla is now demanding to be judged.