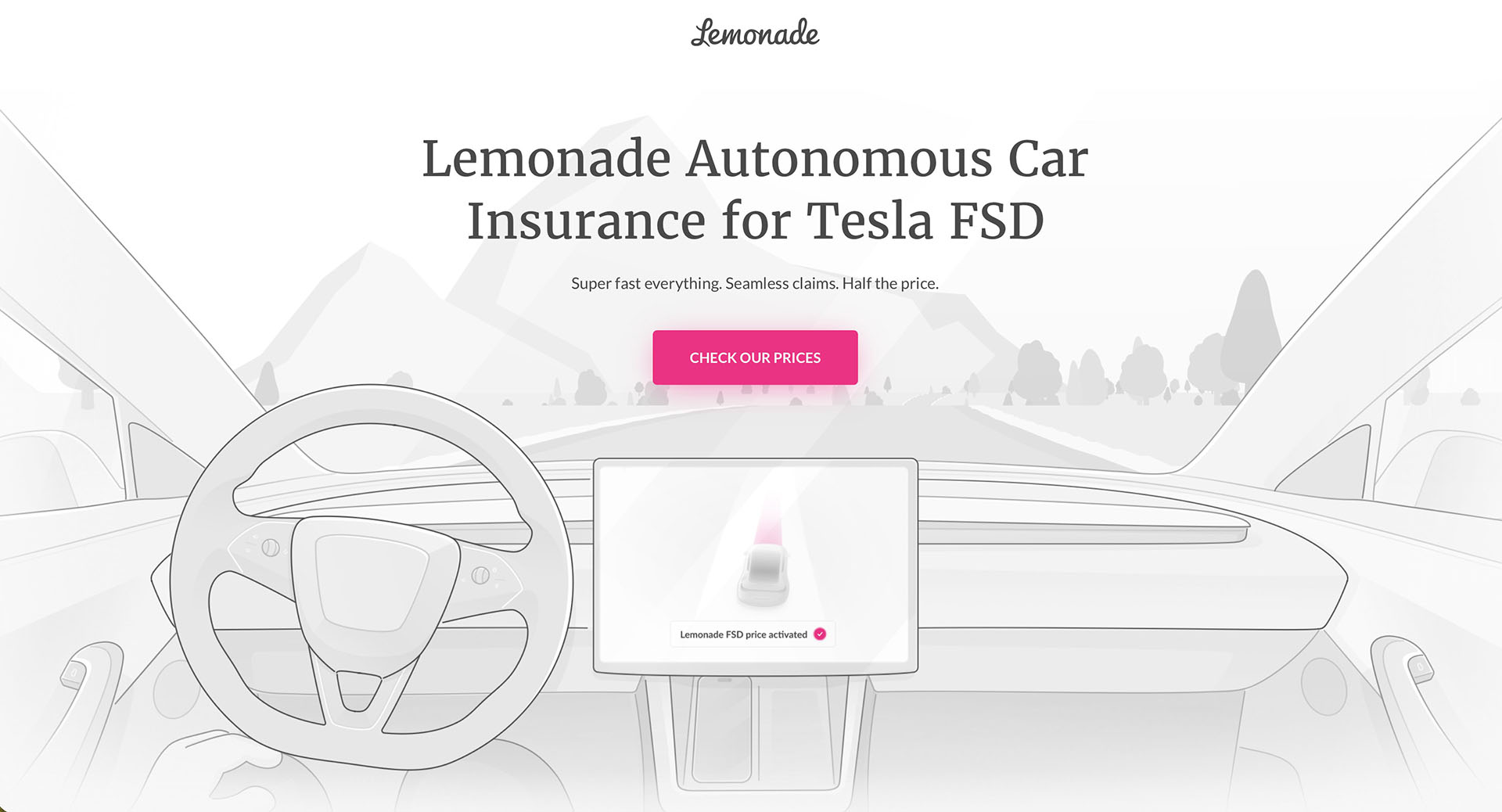

The relationship between advanced driver-assistance systems and insurance premiums has long been theoretical, but one company is now putting a staggering number on it. Insurtech disruptor Lemonade, Inc. (NYSE: LMND) has unveiled a groundbreaking offer exclusively for Tesla owners: a 50% discount on insurance premiums for vehicles using the company's Full Self-Driving (FSD) software. This bold move directly ties the cost of coverage to the perceived safety of automated driving technology, challenging the entire auto insurance model and signaling a potential future where your car's software is as important as your driving record.

A Data-Driven Bet on Robotic Safety

Lemonade's proposition is rooted in a core belief that FSD, despite being a Level 2 driver-assist system requiring constant supervision, fundamentally reduces risk. The company's dedicated webpage, stating "Driving is changing. Insurance should too," frames this not as a simple promotion but as an evolution of risk assessment. Traditional insurers primarily base rates on human driver history, vehicle type, and location. Lemonade is now aggressively weighting a new variable: the presence and active use of a sophisticated AI co-pilot. This discount represents one of the most substantial financial recognitions of autonomous vehicle technology's safety potential by any major insurer to date, effectively betting that Tesla's real-world data will support a significantly lower claims frequency for FSD users.

Disrupting the Traditional Insurance Model

This initiative is a strategic spearhead for Lemonade's entry into the competitive EV insurance space. By targeting the tech-savvy, early-adopter Tesla demographic, Lemonade positions itself as a forward-thinking alternative to legacy providers. The offer turns FSD, a costly $12,000 (or $199/month subscription) option, into a potential long-term value proposition beyond convenience. For a customer paying $2,400 annually for insurance, the 50% discount saves $1,200 per year, potentially offsetting the FSD subscription cost in its entirety. This creates a powerful financial incentive for both FSD adoption and policy switching, leveraging Tesla's ecosystem to rapidly acquire customers.

However, the offer raises immediate questions about verification and liability. Lemonade will likely require proof of FSD capability via the Tesla app and may utilize telematics to confirm its regular use. The critical disclaimer remains that the driver is ultimately responsible, a legal reality that underscores the complexity of insuring semi-autonomous systems. This move pressures other insurers to clarify their stance on ADAS discounts and accelerates the industry's shift towards usage-based, data-intensive pricing models.

Implications for Tesla Owners and Investors

For Tesla owners, this is a tangible monetary validation of their investment in advanced technology. It provides a compelling new argument for purchasing or subscribing to FSD, directly impacting the total cost of ownership. Prospective buyers may now factor in potential insurance savings, making Tesla's vehicles and software packages more attractive. For investors, Lemonade's bet is a significant external endorsement of the safety and economic value of Tesla's autonomy stack. It highlights a future revenue stream where software excellence lowers operational costs for owners, strengthening brand loyalty. As more insurers potentially follow suit, it could create a powerful feedback loop: widespread FSD adoption leads to better safety data, which justifies lower premiums, which in turn drives further adoption, fundamentally reshaping the economics of car ownership and insurance.